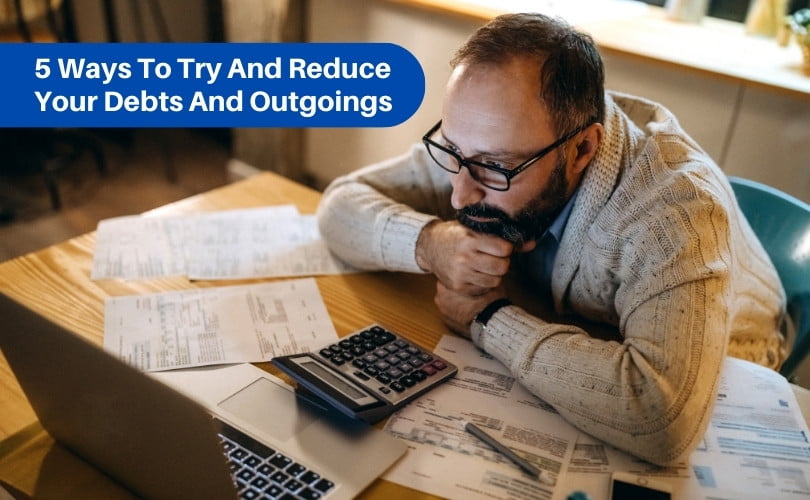

Reducing debts and outgoings is crucial for several reasons. It promotes financial stability, allows for efficient debt repayment, improves credit scores, reduces stress, provides flexibility in managing finances, saves on interest payments, and creates opportunities for investments and future financial goals.

4 Responses

Sir please lona kar dena sir

I just could not depart your web site prior to suggesting that I really loved the usual info an individual supply in your visitors Is gonna be back regularly to check up on new posts

Its like you read my mind! You appear to know a lot about this, like you wrote the book in it or something. I think that you could do with some pics to drive the message home a little bit, but instead of that, this is fantastic blog. An excellent read. I will certainly be back.

Its like you read my mind! You appear to know a lot about this, like you wrote the book in it or something. I think that you could do with some pics to drive the message home a little bit, but instead of that, this is fantastic blog. An excellent read. I will certainly be back.